| Dr. Mahender Singh Meena Deaprtment of ABST Government College, Gangapur City University of Kota (Rajasthan) India. | Sameeksha Agrawal Department of ABST, (Research Scholar) University of Kota, Rajasthan, India |

Abstract

Green banking has become a key element of sustainable finance in recent years, given the rise in importance of environmental sustainability and responsible economic development. Financial institutions are going digital, going paperless, financing renewable energy and financing sustainable practices in India with increased adoption of financial banking practices to fulfil the national sustainable development goal. But lack of awareness and adoption is a big concern when it comes to the effectiveness of these initiatives. The present research paper critically analyses customer awareness and acceptance of green banking products/services in India and their impact on sustainable finance and towards Viksit Bharat 2047. The overall research design for this study was a qualitative, desk study design and secondary data from peer literature, sustainable reports, policy documents and studies from the banking sector from 2019 to 2025 were used. Thematic analysis is used to extract the salient themes concerning customers’ awareness, behavioural patterns while adopting bank products, level of customer satisfaction with digital banking, transformation of banking, integration of fintech, and sustainability measures achieved. The results show that there has been a significant rise in the use of digital banking services, but there is not a high awareness about the importance of green banking for many customers. Convenience, accessibility, perceived usefulness, trust, security, digital banking and fintech innovations are crucial enablers of sustainable banking and are key drivers of customer adoption. The study also highlights regulatory uncertainty, institutional barriers, cybersecurity issues and lack of awareness as major obstacles in the way of implementing green banking. But according to the research, greenhouse gas mitigation efforts must focus on strengthening customer awareness, increasing

digital access, incentivising financial inclusion through fintech and establishing supportive regulations to drive the adoption of green banking. The study fills the gap in the existing literature with an emphasis on customer behaviour, sustainability and digital transformation aspects in the context of the Indian financial system transitioning towards a sustainable and inclusive one to meet the goals of Viksit Bharat 2047.

Keywords: Green Banking, Customer Awareness, Customer Adoption, Sustainable Finance, Digital Banking, Fintech, Environmental Sustainability, Viksit Bharat 2047.

1. Introduction

Sustainability has become a political priority and business strategy for companies, with climate change, environmental degradation and resource depletion having become more serious and worse for humanity. FIs are expected to play a role in supporting sustainable development and environmental protection by incorporating environmental issues into operational and strategic aspects. In this context, green banking has become a significant tool for banks to help promote sustainable economic growth and decrease their environmental impact. Green banking is about environmentally responsible banking that promotes sustainable investment, carbon emission reduction, paperless banking and extends credit for environmentally friendly projects (Desai & Prajapati, 2024). Green banking is a banking approach that puts environmental and social goals into banking operations and decision-making processes, knowing that the traditional banking approach emphasises exclusively financial performance.

The importance of green banking has grown considerably over the last few years, as the financial sector is the central player visible in shaping capital flows in the economy. Banks affect the environmental actions of businesses and people by way of their lending, investment and services to customers. Given the rise in environmental concerns and regulations and increasing institutions’ focus on green banking, this has shifted it from a voluntary sustainability drive to a component of sustainable finance (Desai and Prajapati 2024). Likewise, Sharma and Choubey (2022) argue that promoting green banking helps reduce environmental impacts, build organisational reputation, gain stakeholder approval and improve the sustainability of the banks.

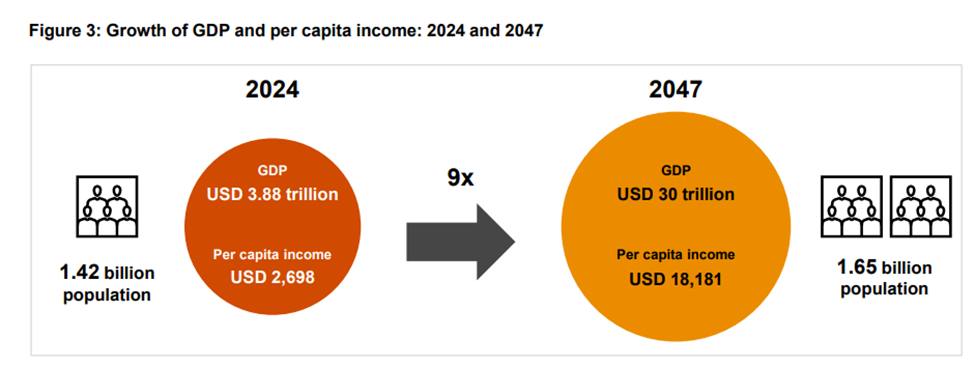

Source: (Viksit banking – A roadmap for the Indian banking sector for 2047 20 th IBA Banking Technology Conference, 2025)

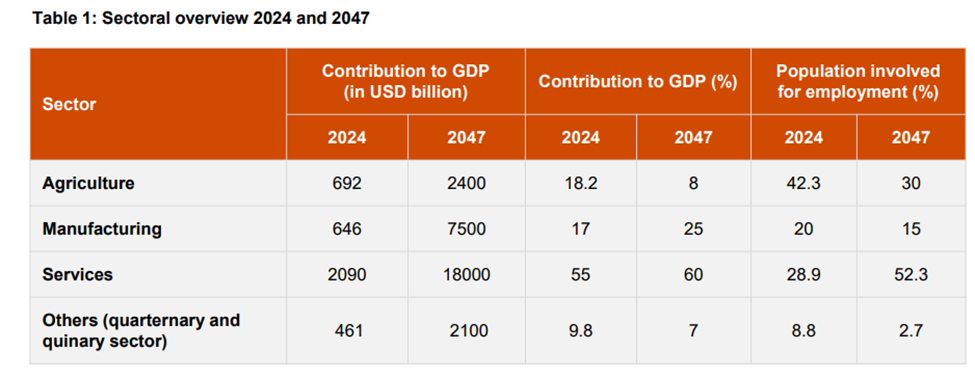

In the context of India’s vision to become a developed nation by 2047, the need of the day is sustainable financial systems and environmentally responsible banking. As per the projections of the Viksit Bharat 2047 vision, the projections of India’s GDP in 2047 were USD 30 trillion from the starting point of USD 3.88 trillion in 2024, and the per capita income would reach USD 18,181 from USD 2,698 in 2024. At the same time, the population is expected to grow from 1.42 billion to 1.65 billion people. Across this sector, the service sector is expected to continue its growth trend, expanding its share of GDP from 55% in 2024 to 60% in 2047 and its employment share from over 52% to more than 60%. This rapid growth in the economy necessitates significant financial intermediation, digitalisation and eco-friendly investments. Thus, the significance of achieving sustainable economic development, utilization of resources, protecting the environment, and keeping in inclusive economic growth has manifested the relevance of green banking as a strategic ammunition for sustainable finance in the larger circle of Viksit Bharat 2047.

Although these have been achieved, customers’ involvement remains a crucial aspect of green banking growth. Even if banks can roll out “green” services and products, they are only as effective as the awareness of the customers about them and their willingness to use them. Hence, this has led to the importance of customer awareness and adoption becoming a critical component of the success of green banking. The findings of Ellahi et al. (2023) reveal that knowledge has a definite impact on customers’ eagerness to participate in green banking services and environmentally friendly financial practices. Similarly, Katti and Jagtap (2022) have found that though banking customers are becoming more exposed to digital banking technologies, they lack awareness of these technologies even now.

1.2 Research Problem

Despite the significant focus on green banking by researchers, financial institutions and policy makers, some issues persist to prevent the mass adoption of green banking. Despite extensive efforts by banks to enhance their digital transformation and sustainable banking programs, many consumers are oblivious to the environmental impacts of the services they utilise (Kumar et al., 2025).

One of the points noted in the literature was that many consumers are involved in digital banking activities without even realizing them as part of green banking. Online banking, for instance, mobile banking, electronic statements and digital payment systems are responsible for a huge portion of the eco-friendliness by lowering paper usage and emissions. But the awareness about these environmental benefits is still low (Ellahi et al., 2023; Katti & Jagtap, 2022). The disparity between the usage and awareness hinders the wider behavioural and environmental effects of GB initiatives.

Moreover, previous research often focuses on awareness, customer satisfaction, digital banking, sustainability, or the adoption of fintech as individual concepts or constructs, and not on a holistic view of them. Chandran et al. (2025) further claim that regulatory ambiguity, lack of uniformity, and institutional obstacles persist in inhibiting the progress of green banking in India. Likewise, Khan et al. (2024) found that trust, security, responsiveness, and reliability create a ground for acceptance of sustainable e-banking services by customers. Therefore, it’s important to have a detailed study of green banking awareness level among the customers and the penetration of the same in the context of sustainable finance and Viksit Bharat 2047.

1.3 Research Rationale

There are three critical factors behind this study. Participation of the customers is essential for any green banking programme to succeed. Environmental attributes of financial services and products can only be achieved once they are actively taken up and used by customers, and financial institutions introduce them. Thus, to make green banking strategies effective, it is important to understand some factors that influence the awareness and acceptance of these strategies.

Secondly, green banking is part of an evolving sustainable finance and environmental governance landscape. Banks can shape sustainable consumption patterns, promote greener investments, and aid in the shift to a low-carbon economy (Desai & Prajapati, 2024). Customer behaviour can be explored to gain insight into how it can be better achieved.

1.4 Research Aim

To critically analyse customer perception and the acceptance of green banking services and their role in attaining sustainable finance and Viksit Bharat 2047 in India.

1.5 Research Objectives

- To understand the level of awareness about customer awareness towards the services offered under green banking in India.

- To explore the factors affecting customer use of services related to green banking.

- To assess digital banking and fintech’s contribution to green banking.

- To assess the contribution of green banking towards sustainable development and sustainable finance.

- To suggest measures to reinforce the adoption of green banking in India.

1.6 Research Questions

- RQ1: To know the present awareness level of customers towards the green banking services in India.

- RQ2: What are the factors that can affect the willingness of the customers to use green banking services?

- RQ3: In what ways do digital banking and fintech innovations support the adoption of green banking?

- RQ4: How does Green Banking contribute towards sustainable finance and Viksit Bharat 2047?

2.1 Concept and Evolution of Green Banking

One of the most important trends in sustainable finance is the rise of what can be called ‘green banking’.inë As financial institutions increasingly hold the responsibility to engage in active management of climate change and sustainable development, the concept of ‘green banking’ has taken root as one of the most prominent challenges of sustainable finance. The traditional view on banks has long been one of a financial intermediary which mobilises savings and enables investment. But the concerns on climate change, environmental degradation, utilization of resources have grown the responsibility of banks beyond mere economic activities. Hence, the concept of ‘green banking’ entails bankers moving away from traditional banking practices and embodying a pro-ecological perspective in their business, product, and policy mix, holding sustainability as a central element of each of their business operations.

According to Desai and Prajapati (2024), green banking is the integration of issues related to environmental, social and governance norms (ESG) in financial decision-making, which helps in sustainable growth and climate resilience. In the same way, Sharma and Choubey (2022) claim that green banking can go beyond paperless transactions and digital banking services to green financing, environmental risk assessment, sustainable investment strategies, and corporate environmental responsibility. The interpretations highlight that green banking is not only a technological development, but an approach shift of banking philosophy as such.

But there are considerable differences over the scope of green banking. Previous research had concentrated mainly on the reduction of paper and the push for electronic banking services (Rai et al., 2019). It has been extended to other areas of sustainable finance such as green bonds, financing of renewable energy, the integration of environmental, social, and governance (ESG) principles, and climate-aware loan policies (Desai & Prajapati, 2024; Chandran et al., 2025). The development of this evolution is an indication that the adoption of green banking has gone beyond operational efficiency to a wider concept of sustainability. Therefore, the concept of ‘green banking in the modern sense’ needs to be considered as a multi-faceted process that includes both environmental commitment and financial performance but also considers the needs and expectations of the client and sustainable development goals.

2.2 Human Resources to Drive the Growth of Green Banking

For grasping customer awareness and receptivity towards green banking services, it is essential to have a firm comprehension of the theories. In the literature, several theories have been used to capture the phenomenon of behavioural intentions, organisational adoption and decision making for sustainability.

The Technology Acceptability Model (TAM) is still one of the most important frameworks for understanding technology adoption behaviour. The TAM study found that customers will be more likely to utilise new technologies if they believe the new technology to be useful and easy to use. In green banking, convenience, accessibility, efficiency, and ease of use are important factors in decision-making processes (Ellahi et al., 2023). The adoption of internet banking, mobile banking and digital payment systems has gained popularity over the years, which makes the relevance of TAM to explain the adoption of green banking look relevant.

The TAM may not fully account for the phenomenon of ‘green banking behaviour’ as the perception of environment and sustainability issues transcends technology issues. Stakeholder Theory expands on this view, noting that organisations need to engage with as many stakeholders as they can, such as customers, regulatory bodies, community, and environmental groups. The study by Sharma and Choubey (2022) illustrates that Indian banks are becoming a hot favourite with their banking activities focusing on green banking to meet the expectations of their stakeholders from this banking paradigm on sustainability and corporate responsibility.

Another dimension of an understanding of green bank adoption comes from the “institutional theory”, which considers the regulatory frameworks, industry norms and pressures. Chandran et al. (2025) point out that regulatory uncertainty and institutional hurdles are highly influencing the rate of green banking adoption in India. From this view, banks may take action on green practices not just in response to customer demand but also because of regulatory expectations or due to competition concerns.

Surprisingly, no single theory can explain the adoption of green banking enough. A critical comparison of these theories indicated that no one theory fully covers the adoption of green banking. TAM eloquently accounts for individual customer behaviour; the Stakeholder Theory is more concerned with providing a framework for the motivations of the organisation, whilst Institutional Theory emphasises the surroundings and controls to which the organisation is subject. Thus, it is important to consider a multi-dimensional approach, as it will be difficult to achieve a comprehensive understanding of green banking awareness and adoption unless this is taken.

2.3 Green Banking Practices in the Indian Banking Sector

The sector has seen notable development in the field of green banking in India during the decade of sensitisation. The recent rise in concerns about the environment, the drive for digital transformation, financial inclusion programs, and sustainability policies have all spurred government banks to become more environmentally conscious. Government banks have been driven to be more environmentally responsible by a range of environmental concerns, digital transformation, financial inclusion programs, and sustainability policies. The public and private sector banks have launched various green banking programs such as paperless banking, mobile banking, internet banking, green loans, financing renewable energy, and sustainable investment products, etc.

Some green banking initiatives taken by the Indian banks are cited by Sharma and Choubey (2022), such as energy-efficient banking operations and management, environmental risk management, green financing programmes, and awareness-building initiatives for bank customers. Likewise, Fakruddin (2025) mentions the initiatives taken up by the State Bank of India for the inclusion of sustainability in the banking sector to handle paperless banking, exchange papers, financing renewable energy and environmentally friendly banking practices.

Despite these schemes, the journey to green banking is still not uniform across the banking sector in India. According to Chandran et al. (2025), the institutional barriers, regulatory inconsistencies, and ambiguity in sustainability standards persist in slowing down the spread of sustainable banking practices. Moreover, many banks continue to focus on short-term financial gains rather than long-term values for sustainability.

2.4 Customers’ awareness of their Green Banking Services

Customer awareness is one of the many factors studied which are closest to meeting the acceptance criteria for green banking adoption. Consciousness is a customer’s awareness and knowledge of products and services, benefits to the environment and sustainability goals. Past studies have clearly shown that customers’ awareness is a key determinant of their attitudes and behavioural intentions.

The research study by Ellahi et al. (2023) concluded that awareness among customers plays a significant role in the acceptance of green banking practices. The study suggests that those who have greater awareness of environmental issues and financial literacy are more inclined to use green banking services. Likewise, Katti and Jagtap (2022) have found that there are wide variations in the awareness of SBI customers concerning the percentage with education, income and occupation.

Kumar et al. (2025) also found that while there has been a rise in the use of digital banking services among customers, there was a lack of awareness regarding the environmental impact of these services. This is important to note, considering that it would seem that in the case of adoption, awareness is not necessarily present. Customers can do green banking activities without realising that they are contributing towards sustainability.

An in-depth study of these studies brings an interesting point into focus: each of them takes a different perspective on the same kind of study. Although awareness is always reported as being a strong factor in the adoption process, most studies have been based on the availability of geographically restricted samples and cross-sectional data.

2.5 Customer Adoption Behaviour and Green Banking

Customer adoption is the level of adoption of green banking products/services by customers. Previous studies suggest that a variety of technological, behavioural, environmental and institutional factors affect adoption.

The presence of awareness results in the positive attitude of the customers towards green banking services, as found by Ellahi et al. (2023). The results of their research back the call for customers to know the advantages of environmentally responsible banking practices. Likewise, Charan et al. (2019) found that customers’ perceptions are generally favourable regarding green banking services, such as Internet banking, mobile banking and electronic banking.

Convenience, time saving and accessibility are highlighted as key reasons for adoption interest (Rai et al., 2019). They also reveal customer concerns about security, privacy and customer-technology complexity as challenges. These findings suggest adoption decisions are a balance between the perceived advantages and perceived disadvantages.

Most critically, many of the studies studied technological factors of adoption without considering other motivational influences of the environment. Convenience and convenience/performance are still important factors, but there may be a growing recognition around the adoption of the issue of the environment. Further investigation should thus take a more holistic approach that spans technology, nature and psychology.

2.6 Customer satisfaction, trust and loyalty

Customer satisfaction is considered one of the key achievements of the implementation of successful green banking. Customers who are satisfied with green banking service will more likely make their vision a reality by continuing to use the service, recommending it to others and building their long-term relationship with financial organisations.

The security, trust, convenience, value creation and environmental responsibility are suggested to be the factors affecting customer satisfaction in green banking by Herath and Herath (2019). Their conceptual framework highlights the multidimensional aspects of satisfaction and underlines the role of balancing technological efficiency with environmental benefits.

Having a similar perspective, Khan et al. (2024) found that major factors influencing satisfaction in a sustainable e-banking environment are efficiency, reliability, responsiveness, safety, and security. The results show that for customer satisfaction to be fulfilled, it is not enough to make an environment sustainable; service quality is still relevant.

Moreover, Adhikari et al. (2025) prove that there is a positive association between green banking practices and customer loyalty through a positive green image. Interestingly, they found that green trust does not have a direct effect on customer behaviour – the direct effect of trust on customer behaviour is commonly suggested as a causal chain, despite these findings.

It showed that green banking was not consistent, indicating that there is a need to investigate further aspects of the mechanism that green banking has on customer loyalty. What seems to be the case is that the customer will react more powerfully to what he or she sees (sustainability measures, the organisation’s reputation, etc.) than to what he or she can’t feel or see (trust, etc.).

2.7 Digital Banking, Fintech and Sustainable Finance

Digital transformation is one of the key factors behind the accelerating spread of green banking. Digital banking helps directly fight against physical infrastructure and paper-based transactions, thereby helping to make bank operations more environmentally friendly and accessible to services.

Chandrasekaran and Narayanan (2024) determined that Indian banking customers’ green banking adoption was positively related to digital transformation. According to their research, the trend of green digital banking services is gaining popularity among customers due to their convenience and efficiency.

In the same vein, the study by Gupta et al. (2025) establishes the important link between sustainable digital banking, green finance and Sustainable Development Goals. Technologies such as artificial intelligence, blockchain, digital payments, and ESG analytics enable financial institutions to boost their sustainability outcomes and broaden their financial offerings for customers. Artificial intelligence, blockchain, digital payments, and ESG analytics are some technologies that help financial institutions achieve better sustainability performance and, at the same time, increase customer access to financial services.

Similarly, Vijay and Karthigeyan (2025) also underscore the contribution of fintech to green financial inclusion. They found that new technologies in financial services can help underserved populations access viable financial products and lower the environmental footprint of conventional banking services.

2.8 Challenges and Barriers to Green Banking Adoption

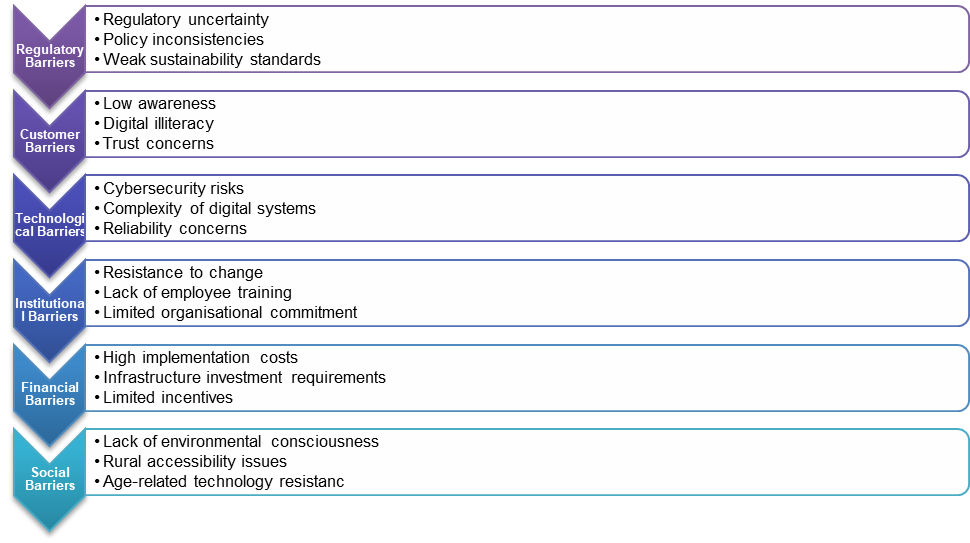

Though green banking is gaining significant momentum, a few barriers are limiting its mainstream adoption. Regulatory uncertainty, institutional constraints, and policy inconsistencies are key impediments to the implementation of green banking in India, according to Chandran et al. (2025). Lack of clearly defined rules could leave banks reluctant to commit to sustainability projects with high upfront investment and unpredictable benefits.

Figure 1: Major Challenges and Barriers Affecting Green Banking Adoption in India

The challenges of limited awareness, cybersecurity concerns, technological complexity and digital literacy challenges persist at the customer level, limiting the adoption of AI (Katti & Jagtap, 2022; Rai et al., 2019). Additionally, Khan et al. (2024) highlight that security, and reliability issues have always been important issues for customers’ acceptance of sustainable e-banking services.

It seems to this author that a literature search cannot remove these obstacles. Adopting green banking needs coordinated action from regulators, financial institutions, technology providers, and customers. Unless the gaps in awareness, institutional limitations and trust issues are addressed, it is possible for the environmental benefits of green banking to go unmet.

2.9 Research Gap

The current literature offers insightful contributions regarding customers’ awareness, adoption behaviour, customers’ satisfaction, innovation in the field of financial technologies and sustainable finance. But the sizes are usually considered separately and are not quite understood holistically. There is very little research that connects awareness, adoption, digital transformation, customer satisfaction, and sustainability outcomes in a coherent manner, especially in the context of the vision of Viksit Bharat 2047 in India.

In addition, most of the empirical evidence comes from a set of specific regions, specific banks or an isolated part of the customer base, which reduces the generalisability of the findings. Therefore, a systematisation of existing works that could add value could develop in a way to critically analyse the intertwined linkages between customer awareness, action and adoption behaviour, digital banking and sustainable finance, and environmental sustainability still exists in the market. This study aims to fill this lacuna by incorporating these factors into the larger fabric of sustainable development and Viksit Bharat 2047.

Furthermore, much of the empirical evidence is derived from specific regions, individual banks, or isolated customer segments, limiting generalisability. Consequently, there remains a need for a comprehensive synthesis that critically examines the interconnected relationships among customer awareness, adoption behaviour, digital banking, sustainable finance, and environmental sustainability. This study seeks to address this gap by integrating these dimensions within the broader context of sustainable development and Viksit Bharat 2047.

A qualitative, desk-based research method is used in this study to analyse and achieve its research goals of studying India’s customers’ awareness and adoption of green banking services and their role in sustainable finance, contributing to the vision of Viksit Bharat 2047. The study solely uses secondary data from peer-reviewed journal papers, sustainability reports, banking business studies, policy papers, academic papers regarding green banking, customer behaviour, digital banking, Fintech’ and sustainable finance. These key sources offer insights into customer awareness, adoption behaviour, customer satisfaction, sustainability outcomes, institutional barriers, and technological transformation, as noted, in the banking sector (Ellahi et al., 2023; Sharma and Choubey, 2022; Katti and Jagtap, 2022; Khan et al., 2024; Adhikari et al., 2025; Desai and Prajapati, 2024; Chandran et al., 2025; Gupta et al., 2025; Vijay and Karthigeyan, 2025; Chandrasekaran and Narayanan, 2024).

The research method used for the study is Document analysis and thematic synthesis, which is used to systematically examine and review the available literature about green banking practices in India and similar developing economies in the context of sustainable banking. The research methodology adopted for the study is document analysis and the thematic synthesis method, which provides a detailed and systematic examination of available documents and highlights themes. Particular focus is placed on Levels of awareness of customers, behavioural drivers of adopting digital banking, factors of customer satisfaction, digital innovation in banking, the effects of adopting fintech on overall financial inclusion, implications for financial sustainability, and fintech regulatory issues. Thematic coding is used to determine the repeated patterns and linkages among the literature, which are then organised into thematic categories such as awareness of greener banking services, adoption behaviour, customer trust, customer satisfaction, digital transformation, fintech integration, sustainable contribution and barriers to implementation. This helps to have an overall perspective and complete understanding of the interconnectedness of the factors affecting green banking adoption, as well as allowing for a fair comparison of results between the various studies.

The analysis also considers policy and institutional aspects like sustainability initiatives taken by Indian banks such as paperless banking, digital transactions, financing renewable energy, and promoting environmentally sustainable banking practices. The frameworks, institutional barriers and policy proposals that are reported in the literature are critically reviewed and analysed to see how effective they are in achieving the goals of green banking. A comparative analysis of progress is also conducted to determine India’s progress against the global initiatives and developments in the field of sustainable finance, ESG integration, digital innovations in banking and environmentally responsible finance practices.

The findings were interpreted with the guidance of the following theories: The Technology Acceptance Model (TAM), the Stakeholder Theory, and the Institutional Theory. TAM sets the groundwork to understand customers’ perception of usefulness and ease of use for green banking service adoption. The Stakeholder Theory not only allows for analysis of how banks react to environmental and societal demands, but it also enables the exploration of how the environment and societal expectations influence banks to implement green banking. The Stakeholder Theory can be used to understand the reaction pattern of banks to environmental and societal expectations, whereas the Institutional Theory is used to understand the influence of regulatory demands, industry norms or organisation structures on green banking implementation. The application of these theoretical frameworks allows for a more nuanced and comprehensive comprehension of how customers behave and institutions adopt these concepts when sustainability is part of the equation.

Secondary resources may only reduce the ability to directly observe the customer experience; several academic and institutional, as well as sector sources, provide the capacity to triangulate to reduce this weakness. A variety of evidence further provides increased credibility, reliability, and comprehensiveness of findings and decreased potential bias due to individual studies. Hence, there is a strong base for the methodology, which helped to critically synthesise existing knowledge and come up with recommendations for policy, institutional and strategic improvements to improve customer awareness and usage of services availed by customers as a green banking instrument for sustainable development and attain the Viksit Bharat 2047 target.

Table 1: Thematic Analysis Framework

| Theme | Description | Key Evidence from Literature | Major Findings |

| Theme 1: Customer Awareness of Green Banking | Examines customers’ knowledge and understanding of green banking services and environmental benefits. | Ellahi et al. (2023); Katti and Jagtap (2022); Kumar et al. (2025) | Awareness positively influences adoption intentions; however, awareness levels remain uneven across demographic groups, and many customers are unaware that digital banking constitutes green banking. |

| Theme 2: Factors Influencing Customer Adoption | Investigates determinants influencing customers’ willingness to use green banking services. | Ellahi et al. (2023); Charan et al. (2019); Rai et al. (2019) | Convenience, perceived usefulness, accessibility, and ease of use are the strongest drivers of adoption, while security concerns and technological barriers hinder acceptance. |

| Theme 3: Customer Satisfaction, Trust and Loyalty | Evaluates how service quality dimensions affect customer experiences and long-term engagement. | Herath and Herath (2019); Khan et al. (2024); Adhikari et al. (2025) | Customer satisfaction is strongly influenced by security, trust, reliability, responsiveness, and convenience. Green banking practices also enhance customer loyalty through a positive brand image. |

| Theme 4: Digital Banking and Fintech Integration | Explores the role of technology in facilitating environmentally sustainable banking services. | Chandrasekaran and Narayanan (2024); Gupta et al. (2025); Vijay and Karthigeyan (2025) | Digital banking and fintech significantly accelerate green banking adoption by reducing paper consumption, increasing accessibility, and supporting financial inclusion. |

| Theme 5: Sustainability Outcomes and Institutional Challenges | Examines green banking’s contribution to sustainable development and barriers limiting implementation. | Sharma and Choubey (2022); Desai and Prajapati (2024); Chandran et al. (2025); Fakruddin (2025) | Green banking contributes to sustainable finance, environmental protection, and Viksit Bharat 2047 goals; however, regulatory uncertainty, institutional barriers, and limited customer awareness remain significant challenges. |

A thematic analysis of the selected literature shows that there are close connections between the key dimensions of the impact of green banking in India, namely, customer awareness, adoption behaviour, customer satisfaction, digital transformation and sustainability outcomes.

4.1 Customer Awareness Remains a Critical Determinant of Green Banking Adoption

Awareness of customers is always cited as one of the most significant predictors of green banking adoption. According to Ellahi et al. (2023), customers’ state of awareness about environmental sustainability and green banking practices is significantly predictive of the attitude’s customers have toward the adoption of environmentally friendly banking services. Likewise, authors Katti and Jagtap (2022) noted that there are some variations in the level of awareness among the customers based on their educational status, income status and demographic characteristics, which means the levels of awareness are not evenly distributed across all the customers.

There is an important contradiction if the literature is checked. Awareness is always recognised as crucial for adoption. There may be more than what customers are aware of in terms of their environmental effects. Kumar et al. (2025) identified that customers have been using mobile banking, internet banking, ATMs and electronic modes of payment regularly, but not recognising them as part of green banking. This discovery throws into question the paradigm that people always have to realise a change in their own environments before they can adopt it behaviourally, as this example indicates that such behaviours can be adopted independently of environmental awareness. It’s a take-home message that Indian banks have done well in the area of digital banking, while not doing as well in the area of communicating the metrics of sustainability. Green banking is therefore still taken up as a “techno-innovation” for its convenience rather than as an “environmental duty”.

Adoption Behaviour is Influenced by Convenience Rather than Environmental Concern

The analysis shows that convenience, ease and accessibility to green banking services are key factors in influencing customers’ decisions to adopt these services, above all in terms of environmental motivations. According to Charan et al. (2019), the overall attitude of customers towards the green banking services is positive due to their convenience and ease of use. Likewise, in the study by Rai et al. (2019), the key factors affecting the adoption of customers are time saving, accessibility and operations efficiency.

The results are indicative of the Technology Acceptance Model, where it has been suggested that perceived ease of use and perceived usefulness contribute to the intention of technology adoption behaviour. Consumers seem to be more willing to use digital bank channels if they streamline transactions and decrease effort. However, the priority is not giving priority to the environment but seems to be second to utility.

This observation leaves boundless questions about the sustainability narrative that is often attributed to green banking. A primary factor motivating customers to switch to green banking may be convenience, not necessarily environmental issues. From a sustainability viewpoint, such results are still positive, though they could be at risk should technology tastes shift or different competitors enter the mix.

Additionally, there is a tendency in previous studies to establish an immediate link between awareness and adoption. But Kumar et al. (2025) and Katti and Jagtap (2022) indicate otherwise. Environmental issues are not the only hurdles; while a customer can be green without being environmentally aware, an environmentally aware customer can still have difficulties with, for example, technology, customer expertise, or customer usability of the product.

4.2 Customer Satisfaction Depends on Trust, Security, and Service Quality

Khan et al. (2024) conclude that efficiency, reliability, responsiveness, security, and safety did have an impact on customer satisfaction in a green and sustainable e-banking context. It is concluded from a series of findings that the customers who were involved in the study view the green banking services in the same way. Based on these findings, it can be justified that the customers studied consider the green banking services with the same consideration given to the regular banking services. This means it is hard to expect to gain broad acceptance if any of the sustainability programs mean changing a service.

The study by Adhikari et al. (2025) is crucial for the identification of a positive relationship between Green Banking practices and Customer loyalty via creating a green image. Interestingly, green trust does not relate directly to loyalty, suggesting that visible green actions undertaken by the firm may be more salient in customer reactions than abstract perceptions of environmental sustainability.

4.3 Digital Banking and Fintech are Accelerating Green Banking Transformation

A common thread in the literature is the impact of digital banking and fintech on the promotion of green banking adoption. Digital transformation and implementation of green banking had a significant positive connection, as customers’ preferences shifted to the digital banking channel for green banking’s implementation (Chandrasekaran & Narayanan, 2024).

Likewise, Gupta et al. (2025) state that sustainable digital banking is also a critical component in addressing environmental sustainability by lowering paper usage, using resources more efficiently and improving access. The AI, blockchain, and cloud technology, along with other paradigm-shifting innovations like digital payment systems, can help the financial sector lower its expenses while fulfilling environmental goals.

4.4 Green Banking Supports Sustainable Development and Viksit Bharat 2047

The last theme that came out from the analysis relates to bringing about a wider impact of green banking concerning the objective of sustainable development. Desai and Prajapati (2024) state that green banking has now become an important aspect of sustainable finance because it helps financial institutions’ goals or objectives to channel more resources towards sustainable financing activities to sustain the economy. Likewise, Sharma and Choubey (2022) highlight the role of green banking in achieving environmental sustainability, corporate responsibility and value creation for stakeholders.

The concept of ‘green banking’ closely resonates with the goals of ‘Viksit Bharat 2047′ that focuses on sustainable development, digital transformation, financial inclusion, and ‘nature protection’. Initiatives such as Indian banks’ promotion of paperless banking, renewable energy financing and digital service delivery play a role in achieving sustainability goals, highlighting the contributions of the banking sector to the national effort, said Fakruddin (2025).

In addition to this, there are significant problems in the literature that bear relevance for the present study. Chandran et al. (2025) identified three main challenges: regulatory uncertainty, institutional constraints, and a lack of a uniform set of sustainability criteria that are affecting the impact of green banking efforts. Likewise, Desai and Prajapati (2024) have identified a lack of familiarity among customers, high implementation fees and contradictory policies as factors that will hamper the adoption of biometric facilities.

Interpretation of these findings indicates that the development of green banking is not just a banking innovation but also a means of national development. Coordinated action from the regulators, financial institutions, technology providers, policymakers, and customers is key to success. Lack of integrated awareness activities, solid legislation, and robust institutional participation could limit green banking’s ability to support Viksit Bharat 2047.

Green banking has become a vital area of sustainable finance and a key tool for banks to play a role in environmental sustainability, financial inclusion and responsible economic development. The results of this study highlight the critical role of customer awareness in driving their adoption of green banking services but note inconsistencies in awareness among customers. The surging digital banking has amplified the applications of green banking communications, but many people do not know the meaning of green banking. The study also shows that the main factors behind adoption behaviours are convenience, accessibility, efficiency, and usefulness, and that the main factors for customer satisfaction are trust, security, reliability, and service quality.

The analysis also points to the transformative potential of digital banking and digitalisation of financial services, namely fintech, in driving green banking initiatives on paperless transactions, making green banking more accessible, and promoting financial inclusion with an added green dimension. But, despite the above, institutional constraints, regulatory uncertainty, cyber security fears, and lack of client awareness remain as a brake on optimal use of green banking initiatives. In summary, green banking can be said to be consistent with India’s goals for sustainable development and the Viksit Bharat 2047 vision, as it encourages environmental protection, technological development, and inclusive economic growth. Hence, concerted actions of policymakers, regulators, financial institutions, and technology providers to build better customer relationships and to ensure maximal long-term benefit for green banking in India are truly recommended.

5.2 Recommendations

- Carry out a green banking awareness campaign across the country, focusing on awareness among customers regarding the green aspects of digital banking and sustainable financial practices.

- Stimulate the implementation of green banking literacy courses in the banks, educational institutions and in the community to boost awareness and engagement of customers.

- Improve regulatory frameworks and create uniform green banking pricing in order to mitigate banking sector uncertainty and propel uniformity of its application.

- Incentivise banks to offer lower or waived transaction charges, points or benefits to their active users of green initiatives banking services.

- Strengthen the cybersecurity framework and protection processes of customers’ transactions regarding concerns about privacy, trust and digital transaction security.

- Encourage more partnerships in the banking sector with fintech initiatives for innovative, available and eco-friendly financial products.

- Emphasise and support greater investments in ‘green finance’ for renewable energy generation, sustainable infrastructure and environmentally friendly enterprises.

- Embed ESG principles and principles of environmental performance more deeply into banking processes, lending and the development of engagement strategies.

- Promote financial inclusion by providing digital and mobile banking channels for stakeholders and to reach rural and underserved people to provide fair access to green banking services.

- Synchronise the actions of the banking sector with the vision of Viksit Bharat 2047 to make ‘green banking’ more impactful for long-term sustainability.

References, Notes and Bibliography:

- Adhikari, G.M., Sapkota, N., Parajuli, D. and Bhattarai, G., 2025. Impact of Green Banking Practices in Enhancing Customer Loyalty: Insights From Banking Sector Customers. Financial Markets, Institutions and Risks, 9(1), pp.195-215. https://armgpublishing.com/wp-content/uploads/2025/04/FMIR_1_2025_12.pdf

- Chandran, R., Chandran, M.S., Achuthan, K. and Sahib, P.R., 2025. Theoretical perspectives on green banking adoption in India: regulatory uncertainty, institutional barriers, and policy solutions. Discover Sustainability, 6(1), p.581. https://link.springer.com/content/pdf/10.1007/s43621-025-01406-3.pdf

- Chandrasekaran, S. and Narayanan, M., 2024. Green banking initiatives in the Indian banking sector: A study on the digital transformation of banking services. Asian Journal of Management, 15(3), pp.271-276. https://www.researchgate.net/profile/M-Narayanan-3/publication/384573672_Green_Banking_Initiatives_in_the_Indian_Banking_Sector_A_Study_on_the_Digital_Transformation_of_Banking_Services/links/66fe1c4eb753fa724d56fcdc/Green-Banking-Initiatives-in-the-Indian-Banking-Sector-A-Study-on-the-Digital-Transformation-of-Banking-Services.pdf

- Charan, D.A., Dahiya, D.R. and Kaur, M.M., 2019. Customers perception towards green banking practices in India. Think India (Quarterly Journal), 22(4), pp.3653-3665. https://www.researchgate.net/profile/Amita-Charan/publication/337137805_Customers_Perception_towards_Green_Banking_Practices_in_India/links/5eff3b5b92851c52d6139536/Customers-Perception-towards-Green-Banking-Practices-in-India.pdf

- Desai, J. and Prajapati, M.J., 2024. Green banking and sustainable finance: Global trends, Indian practices, and future prospects. A Global Journal of Humanities, 7(4), pp.34-43. https://www.gapbodhitaru.org/res/articles/(34-43)%20GREEN%20BANKING%20AND%20SUSTAINABLE%20FINANC%20GLOBAL%20TRENDS,%20INDIAN%20PRACTICES,%20AND%20FUTURE%20PROSPECTS.pdf

- Ellahi, A., Jillani, H. and Zahid, H., 2023. Customer awareness on Green banking practices. Journal of Sustainable Finance & Investment, 13(3), pp.1377-1393. https://www.researchgate.net/profile/Hesan-Zahid/publication/354763741_Customer_awareness_on_Green_banking_practices/links/6204ed5b50d0b450188dd351/Customer-awareness-on-Green-banking-practices.pdf

- Fakruddin, B., 2025. Integrating Sustainability into Banking: A Study of Green Banking Strategies Adopted by the State Bank of India. Science and Society for Sustainable Future, 4, p.49. https://www.researchgate.net/profile/Yogeesh-n/publication/398493556_Science_and_Society_for_Sustainable_Future/links/693849237e61d05b530ce85f/Science-and-Society-for-Sustainable-Future.pdf#page=58

- Gupta, S., Modi, R.R., Das, D. and Sahu, P., 2025. Sustainable digital banking: Exploring the role of fintech in promoting green finance and sustainable development goals. Journal of Information Systems Engineering & Management, 10(3), pp.547-557. https://www.researchgate.net/profile/Anil-Chauhan-14/publication/390741672_Sustainable_Digital_Banking_Exploring_The_Role_of_Fintech_in_Promoting_Green_Finance_and_Sustainable_Development_Goals/links/68650c3439c3583512060c9d/Sustainable-Digital-Banking-Exploring-The-Role-of-Fintech-in-Promoting-Green-Finance-and-Sustainable-Development-Goals.pdf

- Herath, H.M.A.K. and Herath, H.M.S.P., 2019. Impact of Green banking initiatives on customer satisfaction: A conceptual model of customer satisfaction on green banking. Journal of Business and Management, 1(21), pp.24-35. https://www.researchgate.net/profile/Shantha-Herath/publication/330713991_Impact_of_Green_Banking_Initiatives_on_Customer_Satisfaction_A_Conceptual_Model_of_Customer_Satisfaction_on_Green_Banking/links/5c66d55a299bf1e3a5abd366/Impact-of-Green-Banking-Initiatives-on-Customer-Satisfaction-A-Conceptual-Model-of-Customer-Satisfaction-on-Green-Banking.pdf

- Katti, M.V. and Jagtap, M.V.V., 2022. An evaluation of customer awareness towards green banking practices of state bank of India. Journal of Banking Management, 21(2), pp.661-682. https://www.researchgate.net/profile/Vidya-Katti-3/publication/360685938_An_Evaluation_of_Customer_Awareness_towards_Green_Banking_Practices_of_State_Bank_of_India/links/64881d5ab3dfd73b77812b15/An-Evaluation-of-Customer-Awareness-towards-Green-Banking-Practices-of-State-Bank-of-India.pdf

- Khan, A.J., Hanif, N., Iqbal, J., Ahmed, T., Hameed, W.U. and Malik, A.A., 2024. Greening for greater good: investigating the critical factors for customer satisfaction with sustainable e-banking. Environmental Science and Pollution Research, 31(34), pp.46255-46265. https://www.researchgate.net/profile/Ali-Khan-32/publication/372888045_Greening_for_greater_good_investigating_the_critical_factors_for_customer_satisfaction_with_sustainable_e-banking/links/64cd530540a524707b96fc24/Greening-for-greater-good-investigating-the-critical-factors-for-customer-satisfaction-with-sustainable-e-banking.pdf

- Khan, I.U., Hameed, Z., Khan, S.U. and Khan, M.A., 2024. Green banking practices, bank reputation, and environmental awareness: evidence from Islamic banks in a developing economy: IU Khan et al. Environment, Development and Sustainability, 26(6), pp.16073-16093. https://pmc.ncbi.nlm.nih.gov/articles/PMC10159824/pdf/10668_2023_Article_3288.pdf

- Kumar, S., Manasa, J., Madhusudan, M. and Dixit, C.S., 2025. A Study on Green Banking and Awareness Among Customers of Mysuru. Advances in Consumer Research, 2, pp.1114-1123. https://acr-journal.com/article/a-study-on-green-banking-and-awareness-among-customers-of-mysuru-1491/

- Prabhu, N. and Aithal, P.S., 2023. Quantitative ABCD Analysis of Green Banking Practices and its Impact on Using Green Banking Products. International Journal of Applied Engineering and Management Letters (IJAEML), 7(1), pp.28-66. https://papers.ssrn.com/sol3/Delivery.cfm?abstractid=4400242

- Rai, R., Kharel, S., Devkota, N. and Paudel, U.R., 2019. Customers perception on green banking practices: A desk. The Journal of Economic Concerns, 10(1), pp.82-95. https://pmc.ncbi.nlm.nih.gov/articles/PMC8088406/pdf/10668_2021_Article_1426.pdf

- Sharma, M. and Choubey, A., 2022. Green banking initiatives: a qualitative study on Indian banking sector. Environment, Development and Sustainability, 24(1), pp.293-319. https://pmc.ncbi.nlm.nih.gov/articles/PMC8088406/pdf/10668_2021_Article_1426.pdf

- Vijay, L. and Karthigeyan, D.A., 2025. Sustainable fintech: catalysing green financial inclusion in emerging economies in india. Journal of Development Economics and Management Research Studies, 12(26), pp.76-89. https://cdes.org.in/wp-content/uploads/2025/09/8-Sustainable-Fintech-Catalysing-Green-Financial-Inclusion-in-Emerging-Economies-in-India.pdf

- Viksit banking – A roadmap for the Indian banking sector for 2047 20 th IBA Banking Technology Conference. (2025). [online] Available at: https://www.pwc.in/assets/pdfs/viksit-banking-roadmap-indian-banking-sector-2047.pdf.